Multiply your Profits with the Best Staking Plans

Betaminic’s Big Data Based Profitable Betting Systems Can Tell Us What to Bet on, But the Next Question is How Much to Bet. Which Staking Plan Should I Use? Do not miss this article to know the answers to all these questions.

This article is a MUST READ! It will change your betting style forever.

Article updated on 24 October 2024.

A betting system tells us what to bet on.

A staking plan tells us how much to bet.

If we have the right betting system and the right staking plan, we can have high hopes for a successful betting strategy. Betaminic already has the best betting systems, researched and developed in the free to use Betamin Builder Tool, and now the question of “What is the Best Staking Plan?” has been answered by Tom Whitaker in his book The Staking Plans Book available now on Amazon in Paperback and on Kindle.

In the book he analyses 32 staking plans and then ranks them in a fair and comparable way so that the best and worst staking plans can be found. He then combined the best parts of the top staking plans and created a new staking method even better than the others. However, just knowing the best staking plan is not enough, we also need to know the correct settings to use with those plans. Each staking plan has its own chapter that shows the best settings, a walkthrough of how to use it, a simple summary table with pros and cons listed and detailed analysis of the staking plan applied to various types of betting system. Each staking plan was tested with 7 different artificial data sets of 10,000 bets and 1 artificial data set of 60,000 bets with different odds levels. Each plan was also checked with real betting strategies taken from Betaminic. Each of those data sets were also put through 1,000 Monte Carlo Simulations to make sure the results were not just due to luck. All staking plans were ranked based on their efficiency when used with a 100 point bank. It also includes advice on when to take out profit from a system. This is probably the most thorough examination of staking plans ever undertaken.

Now, we can exclusively share the ranking of the top 6 and the correct settings for the best ranked staking plan. We also share three important key points learned from the book.

The Top 6 Staking Plans Ranked

6th Best Staking Plan: i-TSM Staking

This staking plan comes from The Staking Machine software created by David Morris. It takes advantage of consistent betting systems by betting more when a system is doing worse than it has done historically and betting less when it is doing better than it has done historically. For this reason it is of interest to Betaminic Users, but it is more complicated than other staking plans. For example, you can increase stakes by 5% of base if the winning average of the last 20 bets is below the long term trend. You can vary the percentage increase and you can vary the number of bets to judge it over. You can also have staggered increases as the win rate can be judged over the last 5, 10, 20, 30 or 50 bets, and different percentage increases allotted for each period. You can also decrease stakes when above the historical win rate. There is a very wide number of setting possibilities, so research is needed, or you can see the best settings in the book.

5th Best Staking Plan: LP28 Staking

This staking plan introduces an element of recovery to percentage staking. The LP28 stands for Long Priced Series 28. It is essentially a very slow and gradual progressive recovery system. The LP28 series looks like this: 1111111111222222333344455667. An easier way to think of it is 10-6-4-3-2-2-1, which is the number of losses until an increase in stakes occurs. In theory, if you lose 28 bets in a row, it comes to the end of the series and we reset back to the start. But the correct settings are needed to know what percentage of your bank the “1” starting unit is set at, just starting by staking 1% of your bank is not efficient.

4th Best Staking Plan: Percentage Staking

Percentage Staking is easy to use and protects the bank. You bet more as your bank increases and bet less if the bank gets depleted. In The Staking Plans Book research, the old rule of thumb “bet 1% of your bank” was proved to be correct to an extent. But by staking different percentages depending on the average odds of your betting system, even better results can be achieved. Again, the correct settings are needed.

3rd Best Staking Plan: Target Profit Staking

This method focuses on the output, not the input. The stake is adjusted so that a target profit is achieved. i.e. You win the same profit each time whatever the odds are. If there are big odds, you bet less to win the same as betting a large stake on lower odds. Target Profit Staking’s key point is that it varies its stake according to the odds, which means it is risk sensitive. Betting more on safer bets and less on riskier bets. This uses betting capital more efficiently.

2nd Best Staking Plan: Secure Staking

Secure Staking uses different percentages for different odds bands. Since it is odds sensitive, the betting capital is used efficiently. It is simple to use and protects the bank due to its percentage staking aspect.

1st The Best Staking Plan: Whitaker Staking

Whitaker Staking takes the best aspects of Secure Staking, Target Profit Staking and Percentage Staking to create the most capital efficient staking plan ever made. It is much simpler to use than Kelly, LP28, i-TSM or other more advanced staking plans. You don’t need to know your betting history, average odds or even keep records. You just stake according to the odds of your next bet as a percentage of your current betting bank. By staking different amounts depending on the odds, the betting capital is used in the best way. For a more detailed explanation of how this staking plan was researched, please see the book which can be bought as a PDF on his website or is free to Betamin Builder users who have purchased a pack of 100 picks or more. We have permission from the author to reproduce part of that explanation here.

Whitaker Staking balances the risk/reward ratio at every odds level. You can use one shared bank that all your systems use to calculate their stakes from.

To understand Whitaker Staking, there are some key concepts we need to know first.

Statistical Independence and The Gamblers Fallacy

The Law of Big Numbers and Regression to the Mean.

Statistical Independence: If events are statistically independent (like separate football matches), the outcome of one event does not affect the outcome of another. This means that the probability of a particular event (e.g., a match having over 2.5 goals) is the same regardless of previous outcomes.

Gambler’s Fallacy: The belief that past independent events affect the probabilities of future independent events. For instance, thinking that after 100 losses, the next match is “due” to be a win.

This means that the winning probability of selections made by most Betaminic strategies are NOT connected. They DO NOT affect each other in any way. This is Statistical Independence. This means that a long losing run by a strategy does not mean the next matches have a higher chance of being a win. Also, a winning run does not mean that a losing run is then due to balance things out. That way of thinking is called “The Gambler’s Fallacy”. The only thing that is connected are the odds influencing opinions that people have of the fixtures if they are connected by some common factor such as playing on the same day, being part of their same bet type, being part of their betting system, etc. For example, if there were no draws in any of the Saturday 3pm kick-offs all over 300 games in Europe, some people falling into the Gambler’s Fallacy might have the opinion that a draw is due in the 5pm kick-off games, but statistically, there is NO increase in the objective probability of that happening, but subjective odds may be affected by people’s incorrect assumption that a draw is due, which could push the draw prices lower if lots of people bet on them, or they may subjectively view that there is less chance of draws since results suggest a streak of no draws. But these are all just short-term results and do not affect the long-term statistical trends. A number of Betaminic strategies find value in these “Against the Trend” pricing errors the market often sees when it overreacts to recent short-term form. So we should clearly understand that a streak of something NOT happening in statistically independent matches featuring different teams in different leagues does not increase the objective probability of that thing happening in the next fixtures. But it may affect people’s betting patterns which DO affect publicly offered market odds which are a subjective reflection of the perceived value of a specific thing happening.

Simply put, the winning and losing runs of betting strategies come at random. The reason for good results is the VOLUME of bets with positive expected value being placed. This means the longer you follow a Betaminic strategy, the more likely you are to get similar results to the long-term data. That is the “Law of Big Numbers” and its connected concept “Regression to the Mean”.

Law of Large Numbers: Over a large number of trials, the average of the results should converge to the expected value. If your long-term expectation is that 33% of games will be a draw, then as you place more bets, the overall percentage should approach 33%.

Regression to the Mean: If you observe a deviation from the expected outcome over a smaller sample size (e.g., 0% in 100 games), future outcomes are not directly affected by past results. The probability remains the same per event, but over time, the results should average out.

Therefore, if we have a draw betting system with a long-term draw rate of 33%, it is the volume of bets with an average win rate of 33% that pull up low win rate periods (losing runs) to the long-term win rate. There is no corresponding winning period for each losing period. It is just that low win rate periods get diluted by the larger volume of 33%-win rate periods. That means the longer you follow that betting strategy, the more chance you have of experiencing that 33% long term trend rate. The 33% long term draw rate means that over 10,000 bets, 3,333 of them will be draws. So, if there are only 333 draws in the first 5,000 bets (7% draw rate), then it would take 33,333 draws (33%-win rate) over the next 100,0000 matches to bring that long term draw rate back up to 32% with 33,666 draws from a total of 105,000 matches. And after 333,666 draws in 1,005,000 matches, that long term draw rate would be back to 33% purely through volume and not through any corresponding winning streak that counterbalances the losing streak. However, due to simple variance it is likely that there would be a positive variance streak at some point, too. But that is purely random and nothing to do with the previous losing streak. That means the volume of bets with a draw rate of 33% dilutes that unusually low losing streak of 7% draws in 5,000 matches. It may seem like we get winning runs that bring the medium-term draw rates back to 33%, but this is just positive variance unconnected to the previous losing runs.

From this we can conclude that:

- Percentage banks are okay to use. When stakes get reduced after a losing run, we will not end up betting less on an expected winning run that is due because it is NOT due. Every bet is the start of a new betting period. So we should always bet based on our bank size in connection with the expected drawdowns we need the bank to survive from that moment in time.

- Percentage banks are recommended. Since winning and losing runs come at random, we need a bank that can handle the statically expected drawdowns that may occur from that moment in time. So if we started with a 100 point bank, and it has been reduced to 50 points, we should base our next stakes on that 50 point bank, not on the 100 point bank. This is because we are starting a new betting run each time we place a bet and should look at the current bank, not the previous bank levels. Percentage staking allows the bank to protect itself when we hit a losing run, that will definitely come at some point.

- Betting events are mostly statistically unconnected, so we can have one mixed bank that all bets from any sport are used on. It does not matter that they are from different sports. Odds are odds, whatever the sport.

Estimating drawdown from implied the win rate using the ELS method

To manage our bank, we need to have an idea of the expected drawdown that could occur. We can do this with historical data like the Betamin Builder shows us. It tells us the maximum drawdowns since 2012. But we also have strategies without historical data, such as selection methods that use Betaminic’s tennis statistics, basketball statistics, ShootingBets or Betlamp. How do we estimate the possible drawdowns for these?

There is another method for estimating drawdowns and that is the Expected Losing Sequence (ELS) method. The Expected Losing Sequence is the number of consecutive, unbroken losing bets in a row that a betting strategy may have. This figure can be calculated using the win rate of a betting strategy and the number of bets we are want to calculate for.

For example, if the win rate of a betting system is 50% (such as for flipping head for a coin) and we plan to flip the coin 1,000 times, then the ELS would be about 10 losing flips in a row. That does not mean that 10 losing bets in a row WILL happen, it just means that it would not be statistically unusual for such a losing run to happen. It means we should plan that any staking plan we have needs to be able to survive such a losing run, especially considering it is expected to happen!

But we most remember that it is perfectly possible for strategies to have losing runs in quick succession. The next question is how many losing runs in a short space of time do we need to plan for without making stakes so low that the bank becomes inefficient with our betting capital. So we know that the estimated drawdown of a strategy can be based on a multiple of the ELS.

You can use the long-term win rate of a betting strategy to calculate its ELS, but we can also use the odds of the next bet to calculate the implied win rate of bet. In fact, it is more efficient to do things that way. One betting strategy has bets at a variety of odds. The average win rate may be 50% but some bets will bet at 1,50 odds and others at 3.00 odds. It does not make sense to bet the same amount on such different odds. Each of those odds has a different implied win rate. With Whitaker Staking, we apply the staking calculation to the odds of EACH bet, so that that stake size is calculated as if we were betting on those same odds 1,000 times and the ELS for just that odds level. This is much more efficient.

How do you calculate the ELS and the Whitaker Stakes?

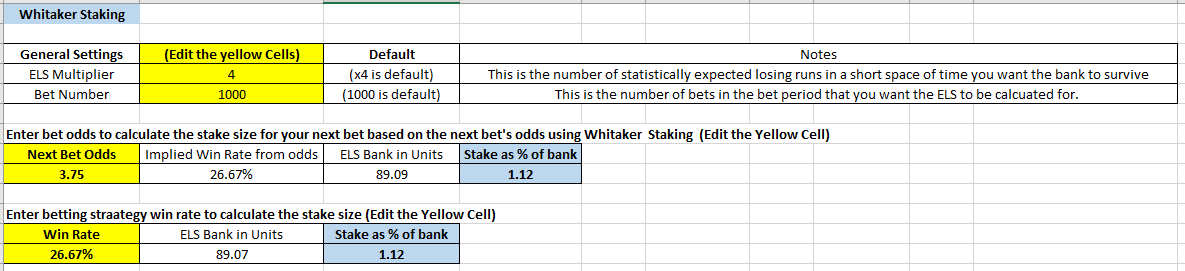

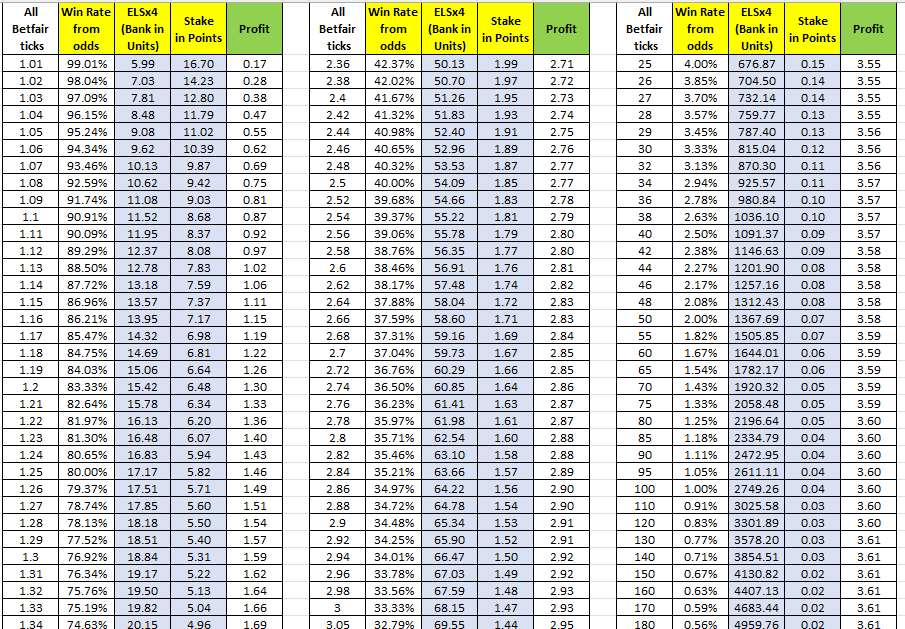

You can refer to this Excel file to get the Whitaker Staking values for each odds level.

Simply edit the yellow cells as needed.

Enter the odds of your next bet or the win rate of your strategy to get the stake %.

You can also edit the ELS multiplier and the Number of Bets you want to calculate the ELS for.

There is an easy reference table for Whitaker Staking ELS4-1000 for back betting and also for lay betting in the excel file. The reference tables are the values for a bank to survive 4 expected losing runs in quick succession over a period of 1,000 bets. Tom would call it a standard betting bank management risk level. If you want to calculate values for more conservative bank management using an ELS x5 or x6, or for longer bet periods of 10,000 or 100,000 bets, then you will need to edit the cells or edit the formula and use a spreadsheet like Excel.

The basic Excel formula to calculate ELS is:

Excel formula: =(LN(n)/-LN((1-(wr))))

LN = a function that returns the natural logarithm of something

n = number of bets

wr = win rate

The win rate can be the historical average of a system or the odds implied win rate of the next bet. Whitaker Staking uses the implied win rate of the next bet to calculate stake size.

Why does Standard Whitaker Staking choose ELSx4 over 1,000 bets for the estimated maximum potential drawdown?

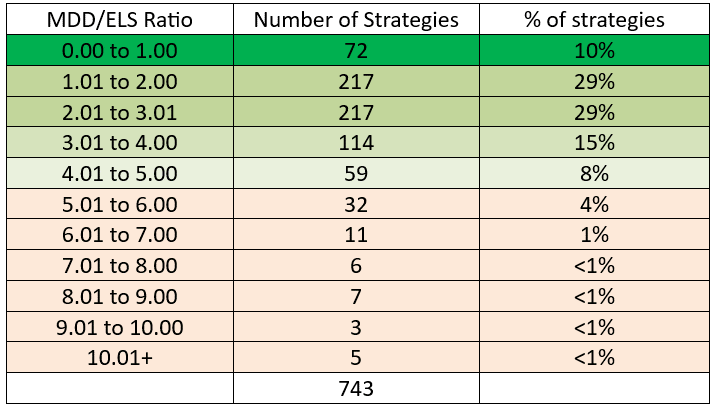

The current standard version that Tom is using calculates the correct stake to be able to withstand the expected losing sequence x4 of a certain odds level over the next 1,000 bets. He investigated 743 public Betaminic strategies and made a simple volatility index showing their maximum drawdowns as a multiple of their ELS.

It showed that 83% of Betaminic public strategies had Maximum Drawdowns (MDD) that were of an ELSx4 or less. The remaining 17% had MDDs over 80 and it was obvious they were high drawdown strategies from their historical MDD. This is why he feels the ELSx4 figure is a reasonable and conservative way to calculate a unit bank for a strategy. In theory, you could make your staking plan more aggressive by using an ELSx3 for bank calculations (68% of Betaminic public strategies could probably survive with that bank size), and you could also make your bank even more conservative by using an ELSx5 for bank calculations (91% of Betaminic pubic strategies could probably survive with that bank size), and so on. It is about trying to find the right balance for your risk comfort levels between bank protection and capital efficiency. You can also change the number of bets in the period you want to calculate for. 1,000 seems like a reasonable number, but you may want to increase that to 5,000 or 10,000 if you have larger volume betting systems.

This means we can now calculate the ELSx4 unit bank for the odds level of that specific bet. The stake size gets adjusted to the risk level of that bet, and also to a level that is meant to survive the expected variance for that odds level over the next 1000 bets. That ends up with the long staking table at the end of his book. This is Whitaker Staking.

In summary, Whitaker Staking bets more on low odds and less on high odds.

It bets a different percentage of the bank on each odds level. For example:

It will stake 3.98% of the bank on a bet if the odds are 1.50.

It will stake 2.51% of the bank on a bet if the odds are 2.00.

It will stake 1.85% of the bank on a bet if the odds are 2.50.

It will stake 1.47% of the bank on a bet if the odds are 3.00.

It will stake 1.04% of the bank on a bet if the odds are 4.00.

It will stake 0.48% of the bank on a bet if the odds are 8.00.

These all seem like very sensible numbers.

You will have to see the excel file for the full set of stake levels.

The staking % is calculated using the odds inferred win rate to calculate the ELSx4 (Expected Losing Sequence) for that odds level. Each odds level effectively gets its own ELSx4 calculated unit bank. The ELSx4 is Tom’s conservative bank calculation so that at each odds level the bank can survive 4 expected losing runs happening in quick succession. This is hopefully enough for most betting strategies.

A Shared Bank for all bets with Percentage Staking

Due to statistical independence, our next stake should always be calculated at the right stake size for the bank at this moment. Each bet is unconnected, so it could come from a Betamin Builder strategy bet, a ShootingBets alert, a Betlamp alert, a Betaminic tennis statistics selection or any other bet with long term positive value. One bank does not need to be exclusively kept for one system.

This means that all bets, from all your betting strategies, can share the same bank if they are using Whitaker Staking. Since it is actually already giving each odds range its own ELSx4 unit bank to avoid going bankrupt over a 1,000 bet period. But you do have one big decision. Do you link your Whitaker staking to your current your cumulative balance (LC) or to your starting bank (NLC).

NLC means “Not Linked to Cumulative” bank balance i.e. constant stakes based on a percentage of the starting bank.

LC means “Linked to Cumulative” bank balance i.e. stakes are based on a percentage of the current betting bank balance.

LC or NLC? Link to Cumulative Bank (LC) or not (NLC)?

If we link the staking plan to the cumulative bank (LC), then it allows you to commit a fixed amount to the system and not have to refill. If you get winning runs, then your bank will increase very quickly and make more money than the NLC version, BUT once you have a high balance, you could still see that drop by 50% on a bad run, so you are always risking all of your bank. More risk for more gain over the long term.

If we don’t link the staking plan to the cumulative bank (NLC), it is risky in the short term if you hit several losing runs and your bank gets reduced a lot. But it will rebound quicker from early losing runs since it does not reduce its stakes. AND, the longer you follow the system, the safer your bank will be as losing runs will probably only affect your profit after you hit the 1,000 bet mark. Less risk for less gain over the long term.

Tom recommends using LC for capital building mode, and NLC for income producing mode.

He also recommends always using LC when your bank is under its starting level, but changing to NLC once it is in overall profit with a large bank. In this way, once you get into significant profit, your bank gets safer and safer, and one bad losing run will not reduce the entire bank by 50% they way LC could.

So, in summary,

Small banks trying to grow quickly = Whitaker LC Staking

When a large bank is under 100% of its starting level = Whitaker LC Staking

When a large bank is over 100% of its starting level = Whitaker NLC Staking

Three Important Key Points Learned From the Book

1 Adjust Stakes to Odds

It is important to adjust the stake size to match the risk of bets. It is inefficient to use one blanket staking rule for all odds, such as the common rule of thumb “bet 1% of your bank and never bet more than 5%”. It is much more efficient to use a staking plan that varies the size of stakes in direct relation to the odds of the bet (Whitaker Staking), or to use different staking plans for different odds brackets to indirectly vary the size of stakes in relation to the odds. In the very simplest terms, bet more on lower odds and bet less on higher odds.

2 Don’t Increase Stakes to Chase Losses

Avoid simple recovery plans that increase stakes in direct connection to previous lost bets in a simple progressive recovery plan. (See our article: Martingale, Fibonacci and other staking plans you should not use.) That kind of stake focussed recovery betting ends up being less efficient as the initial stake levels are pushed lower to avoid bankruptcy later on, so the overall profit will be lower than with other non-recovery staking plans. Also, don’t use ratchet staking as this is recovery by another name and you can end up placing larger stakes than is safe for your bank size after a run of losses.

3 Understand the Key Laws of Statistics

Winning and losing runs come at random and are not connected. We are never due a winning or losing run to counter the other. It is the volume of bets that help return a strategy to its long-term win rate. We have a better chance of achieving similar results to the historical trend the longer we follow a strategy. We must decide a bank management plan that can survive our expected maximum drawdown for the number of bets we expect to place.

What does this mean for Betaminic users?

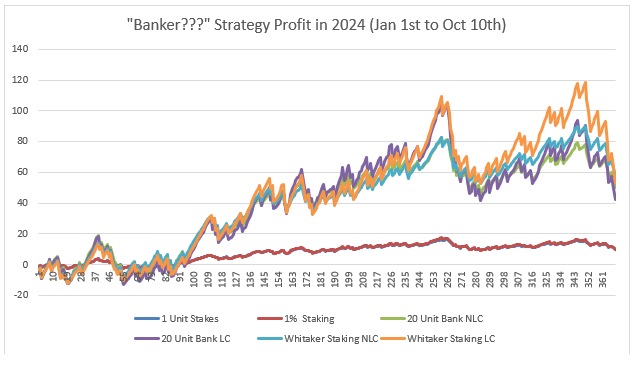

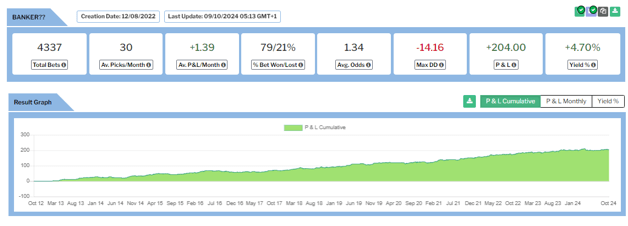

Whitaker Staking applied to Betaminic strategies can multiply profits and use your betting bank capital in the most efficient way. Let’s look at an example staking analysis of the popular “Banker???” strategy.

Back the Home Favourite football Betting Strategy “Banker???” Staking Analysis

After 361 bets in 2024 from January 1st to October 10th, we got these results:

LC means “Linked to Cumulative” so the stake size calculation is adjusted in proportion to the bank changing.

NLC means “Not Linked to Cumulative” so the stake size calculation is constant and does not change as the current bank balance does.

The Unit Bank size is based on its long-term average win rate which is input into the ELSx4 calculator to survive 1,000 bets without going bankrupt.

The difference a good staking plan makes is huge. Whitaker Staking improved level stakes 4.66 unit profit massively to a 59% increase on the bank.

In the graph below we can see the profit journey for each of staking plans over 2024.

Whitaker LC and NLC are pretty similar, but NLC reduces the ups and downs slightly.

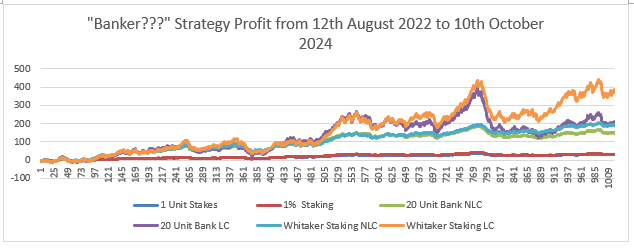

When we apply the staking analysis to all 1,020 results since the strategy was first shared on 12th August 2022, then we get:

This time Whitaker LC Staking clearly beats out NLC.

It increases the level stakes +29 unit profit to a +369% increase on the bank.

This strategy has been performing well and consistently over the long term and is worth considering adding to your portfolio of betting strategies.

You can view and follow the strategy in the Betamin Builder here:

https://www.betaminic.com/system/strategy/details/953067

If you have any questions about Whitaker Staking or want to get Bf Bot Manager files with Whitaker Staking setup, please feel free to contact Tom Whitaker at be*****************@***il.com

| Betaminic Betting Strategies + The Best Staking Plans = The Best Betting Systems |

Sign Up for free to access the Betamin Builder here.

See the Staking Plans that you should NEVER use

Access Betlamp, the amazing free statistics tool here.

See more Betaminic Books here including a free eBook.

See the best betting systems ranked by profit, ROI and risk here.

Read more about the free Betaminic Public Strategies here.

Comments 0

john wayle

February 17, 2024AI should be able to state the next bets stake on any part of an accumulating bet be it say a heinz. l have bets based on late money . Be it 5 mins

or 1/2 hr. l would then know QUICKLY based on a figure given me thanks to AI the sum you stake on the next part of say the heinz or any other common multiple acca. l have days when l can achieve 6 from 7 and once or twice 8 from 8 once or twice a month IF l had AI do the spade work